Financial Services Email Signature Compliance Requirements (2026)

Discover the mandatory requirements financial services email signatures must comply with - disclosure content, retention obligations, and how they are enforced

Short answer

What are the mandatory email signature requirements for financial services?

Email signature compliance in financial services requires regulatory status disclosures, registration numbers, and activity-specific disclaimers in every outbound email. US broker-dealers fall under FINRA Rule 2210 and SEC Rule 17a-4; UK firms under FCA GEN 4 Annex 1; EU investment firms under MiFID II Articles 16(7) and 24. Requirements vary by jurisdiction, regulated activity, and employee role.

Get expert guidance on financial services signature compliance →

Regulatory Exposure

The regulatory cost of absent email signature disclosures

Missing regulatory disclosures in financial services email signatures aren’t a formatting problem. The FCA, FINRA, and SEC treat absent or incorrect disclaimer language as compliance failures subject to censure and fines.

The problem isn’t knowing what to include. It’s guaranteeing it appears in every email, from every employee, on every device.

“We need to make sure that compliance-wise, we’re checking all the boxes signature-wise.”

— Compliance officer, regulated financial institution

Policy documents don’t check that box. Technical enforcement does.

Regulatory Landscape

Which regulations govern email signature compliance in financial services?

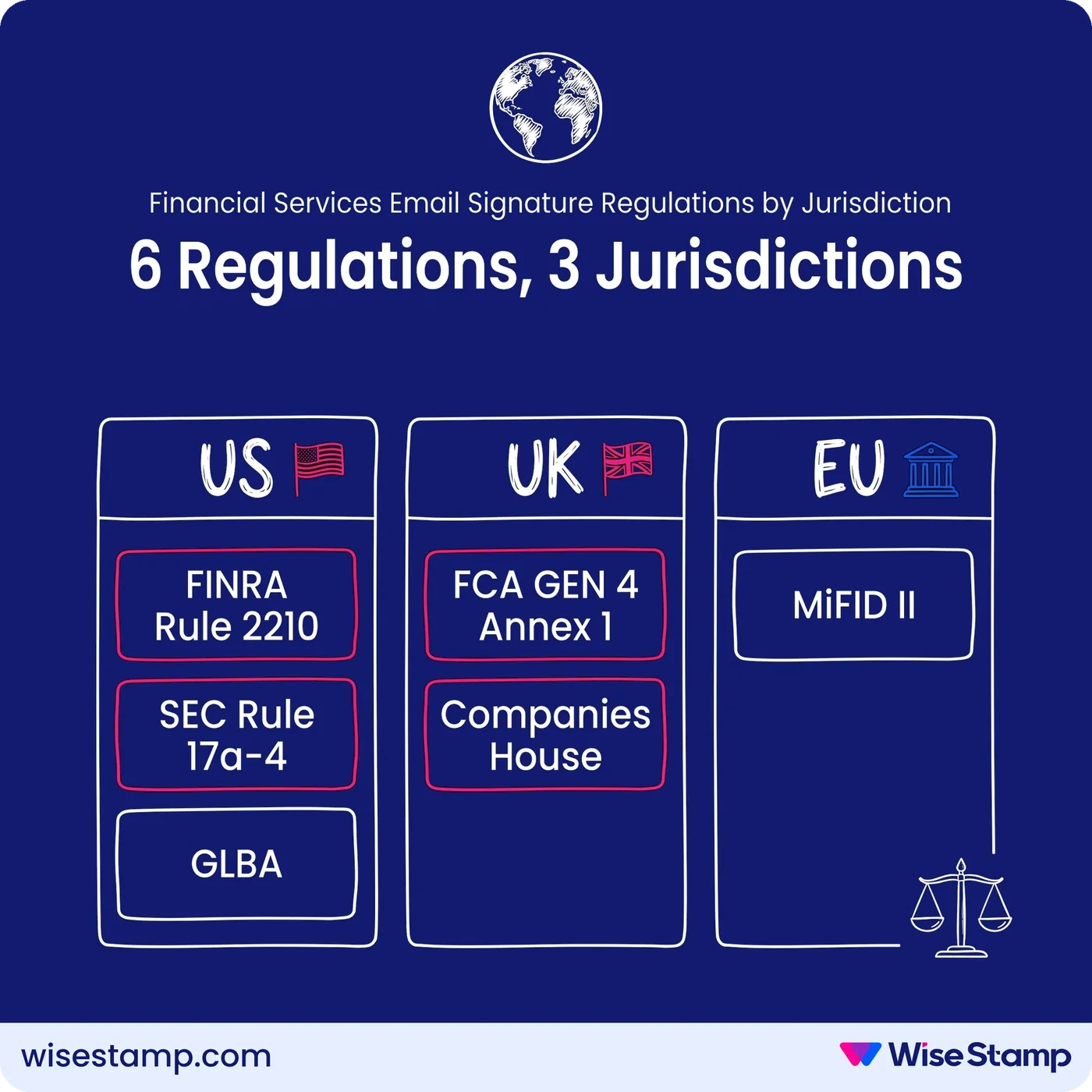

Email signature compliance in financial services spans 4 major regulatory frameworks, depending on jurisdiction and business activity.

| Jurisdiction | Regulation | Primary obligation |

|---|---|---|

| US (broker-dealers) | FINRA Rule 2210 + SEC Rule 17a-4 | Fair, balanced communications; retain all emails min. 3 years |

| US (investment advisers) | SEC Rule 206(4)-1 | No false or misleading statements; disclose conflicts of interest |

| US (all financial firms) | GLBA | Safeguard consumer financial information; privacy policy accessible to clients |

| UK | FCA GEN 4 Annex 1 | “Authorised and regulated by the Financial Conduct Authority” + FRN in every email |

| UK (limited companies) | Companies House | Registered number, registered office, “Ltd” designation |

| EU (investment firms) | MiFID II Articles 16(7) and 24 | Fair, clear, not misleading; risk warnings at equal prominence; records retained 5–7 years |

FINRA Rule 2210 classifies firm communications into 3 categories and requires all client-facing interactions to be fair and balanced.

SEC Rule 17a-4(b)(4) mandates that broker-dealers retain copies of all sent email communications for a minimum of 3 years, with the first 2 years in easily accessible form.

FCA GEN 4 Annex 1 mandates specific statutory disclosure language in every business email from UK-regulated firms.

MiFID II Article 16(7) requires EU investment firms to record all relevant client communications and retain records for 5 years, or up to 7 years upon regulatory request.

Mandatory Content

What must appear in every financial services email signature?

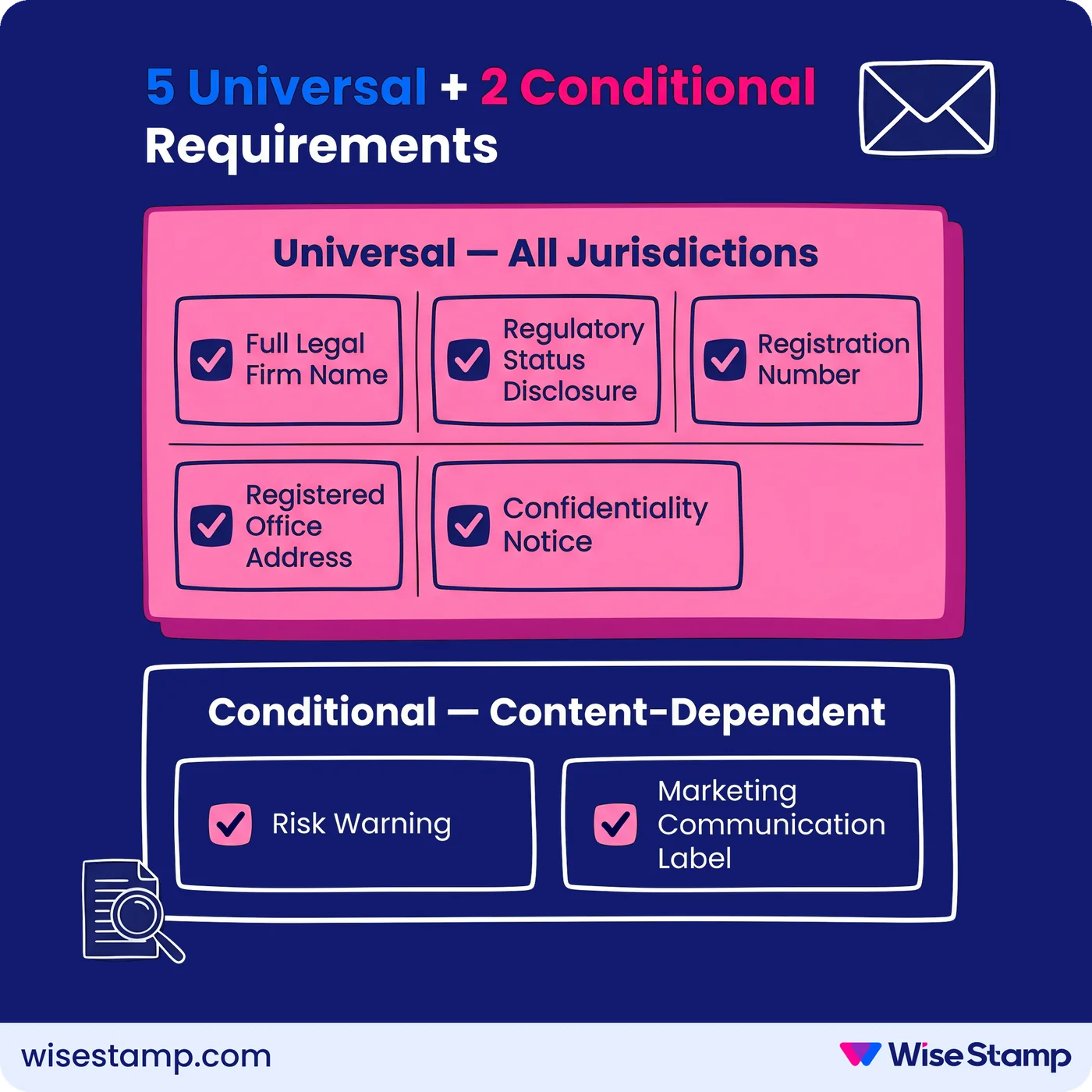

Email signature content requirements vary by regulator, but 5 elements appear consistently across jurisdictions:

- Full legal firm name: Required by FCA, FINRA, and Companies House. Must match the firm’s registered name, not a trading name alone.

- Regulatory status disclosure: FCA mandates “Authorised and regulated by the Financial Conduct Authority” verbatim (GEN 4 Annex 1). US broker-dealers must clearly identify FINRA membership on client-facing communications.

- Registration number: UK firms must display the Financial Reference Number (FRN). US broker-dealers typically include their CRD number. Appointed representatives must display the principal firm’s FRN.

- Registered office address: Required by Companies House for UK limited companies in all business communications.

- Confidentiality notice: Not legally mandated in most jurisdictions, but expected as standard practice in financial services and routinely examined by regulators and legal counsel.

2 elements are conditionally required, depending on email content:

- Risk warning: MiFID II Article 24 requires any email referencing investment benefits to carry a risk warning with equal visual prominence to the benefit described.

- Marketing communication identification: Both MiFID II and FINRA Rule 2210 require that promotional content is clearly labeled as a marketing communication.

Department Requirements

Which financial services employees need different email signature disclaimers?

Disclaimer requirements in financial services differ by role, not just by firm.

A single uniform signature template creates compliance gaps wherever it doesn’t match the regulated activity of the individual sending the email.

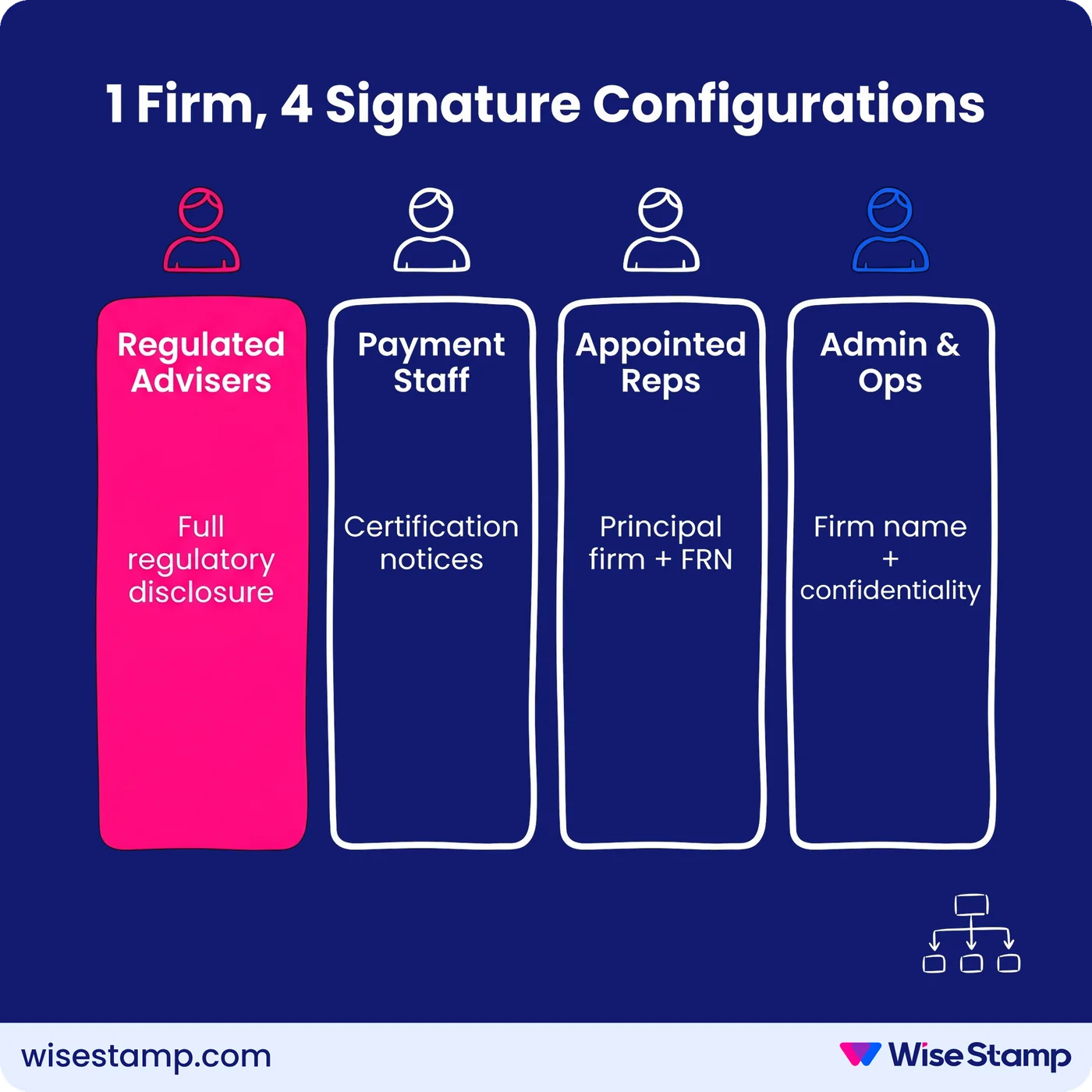

3 employee categories typically require distinct signature configurations:

- Regulated advisers and brokers: Full regulatory status disclosure, registration number, and risk warnings where applicable.

- Payment-collecting staff: Multiple jurisdictions require that employees who collect payments on behalf of clients display specific certification and compliance notices in their communications.

- Appointed representatives: FCA rules require a distinct statement: “[Name of AR] is an appointed representative of [principal firm] which is Authorised and regulated by the Financial Conduct Authority” (FCA GEN 4 Annex 1). The principal firm’s FRN must appear, not the AR’s.

Non-regulated administrative and operational staff don’t require the full regulatory disclosure stack. They still need the firm name, confidentiality notice, and any Companies House-mandated information.

Enforcement Failure

Why does voluntary email signature compliance fail in financial services?

Voluntary compliance fails for a structural reason: it depends on every employee maintaining the correct signature version on every device, and updating it manually whenever regulatory language or firm details change.

“With hundreds of users, you simply cannot rely on people to keep their own signatures updated and consistent.”

— IT professional, compliance community

FINRA and FCA examiners don’t accept “we sent an all-staff email asking everyone to update” as evidence of compliance governance.

Demonstrable, consistent application of required disclosure language, across every outbound email, is the standard regulators expect.

Technical Enforcement

How do you enforce email signature compliance across a financial services organization?

Technical enforcement of email signature compliance requires centralized deployment: signatures designed once and pushed across the organization, with no copy-paste dependency and no reliance on individual employee action.

3 capabilities are non-negotiable for financial services:

- Field-level locking: Regulatory disclaimers, FRN, firm name, and authorized disclosure language must be locked by the administrator. No employee can modify or remove them.

- Department-based templates: Regulated advisers, payment-collecting staff, and appointed representatives need different signature content. Template assignment must be group-based, not left to individual discretion.

- Audit logs: Regulators require demonstrable proof that required content was present and consistent. Time-stamped logs showing who changed what, and when, satisfy this requirement.

WiseStamp’s Role-Based Access Control (RBAC) provides the controls financial services compliance requires.

Admins lock disclaimer fields, registration numbers, and regulatory disclosure language as immutable template elements.

Employees update permitted personal details through the Employee Hub — phone number, photo, direct line — but the compliance layer stays off-limits to individual editing.

Directory sync with Microsoft Entra ID (Azure AD) or Google Workspace keeps employee data and role-based template assignments current automatically.

When a staff member moves from an unregulated role to a regulated adviser role, the correct template applies without manual intervention.

New hires receive a correctly configured signature from their first email, with no IT action required.

For firms running a security review: WiseStamp holds SOC 2 Type II, ISO 27001, and ISO 27018 certifications.

A GDPR Data Processing Agreement is available for EU and UK-regulated firms.

WiseStamp’s server-side deployment adds signatures after send and never reads or stores email content — a requirement financial services IT security teams consistently verify during vendor procurement.

Vendor Evaluation

What capabilities should financial services firms require from email signature management vendors?

Email signature management vendors differ substantially in how well their architecture supports financial services compliance.

Before evaluating design features, verify that the vendor meets the following technical requirements.

| Capability | Why it matters for compliance |

|---|---|

| Field-level locking | Prevents employees from modifying or removing regulatory disclaimers |

| RBAC with distinct compliance roles | Compliance, IT, marketing, and HR each need different permission levels |

| Audit logs | Time-stamped change history with user identity satisfies regulatory examination requirements |

| Department-based templates | Regulated and non-regulated employees require different signature content |

| Directory sync (Entra ID / Google Workspace) | Keeps employee role assignments and registration data current automatically |

| Retention-safe server-side deployment | Adds signatures after send without modifying the original email retained for recordkeeping |

| SOC 2 Type II + ISO 27001 | Required for enterprise procurement and regulated-industry security review |

| GDPR compliance + Data Processing Agreement | Required for EU and UK-regulated firms |

| SAML SSO + SCIM provisioning | Enterprise identity management standard for regulated firms |

WiseStamp satisfies all 9 of these requirements.

Firms conducting a formal compliance review can request the security package ℔ SOC 2 Type II attestation, ISO 27001 and ISO 27018 certificates, GDPR Data Processing Agreement, and architecture diagram ℔ via the WiseStamp Trust Center.

Takeaway

Email signature compliance in financial services: the full picture

Email signature compliance in financial services is not a one-time template exercise.

It requires the right content, enforced technically, with department-level granularity, and an audit trail that holds up under examination.

The mandatory components span:

- Regulatory status disclosure and registration number (FCA FRN, CRD number, or FINRA membership identification)

- Activity-specific disclaimers and risk warnings for regulated employees

- Distinct signature configurations for regulated advisers, payment-collecting staff, and appointed representatives

- Field-level locks that prevent unauthorized edits to compliance content

- Audit logs satisfying SEC Rule 17a-4, FCA GEN 4, and MiFID II Article 16(7) record-keeping requirements

- A vendor with SOC 2 Type II, ISO 27001, and GDPR certifications to satisfy regulated-industry procurement requirements

Manual signature management doesn’t meet this bar. Financial services organizations that rely on copy-paste templates are accepting a compliance gap with every message their team sends.